ONE - quarterly review and a top 10 US health system now in direct negotiations

Our Medical tech Investment Oneview Healthcare (ASX: ONE) has released its March Quarterly Report yesterday.

The two notable points from the quarterly for us included:

- A$19M raised - Tranche 1 of A$12M settled in the quarter (Tranche 2 of A$7M subject to AGM approval in September) - which we took part in

- The Top 10 US health system with 85+ hospitals and 15,000+ beds is now in direct negotiations with ONE on “the scope and timing of the initial project”

That second point is an item that we have been awaiting to hear progress on.

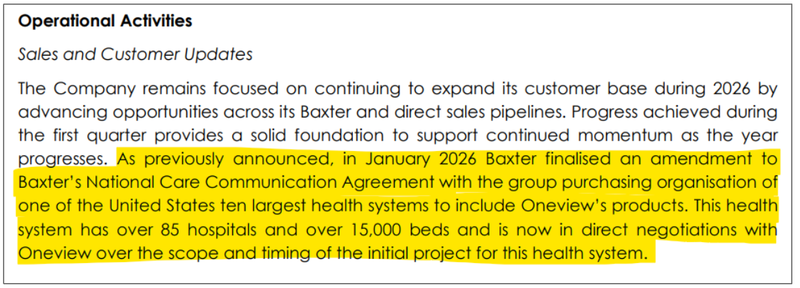

When we last covered ONE’s quarterly back in January, the news was that ONE’s products had been added to the National Care Communication Agreement of one of the Top 10 US health systems via its $13BN partner Baxter International.

This move had opened up potential access to 85+ hospitals and 15,000+ beds.

The next step we wanted to see was that access converting into actual conversations about deployments.

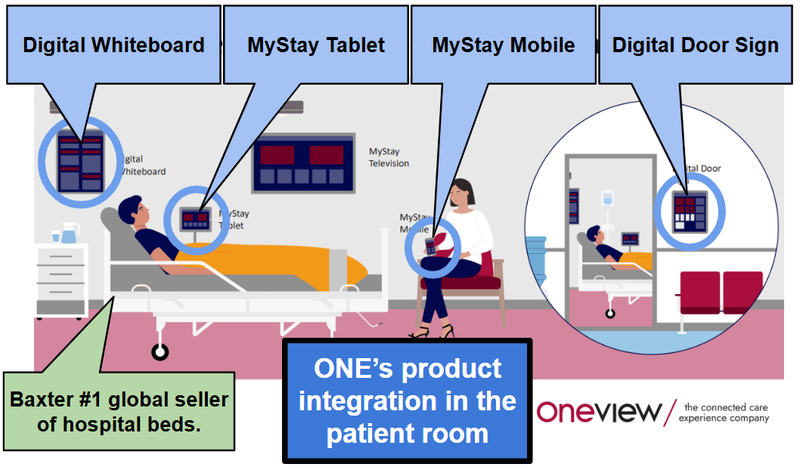

Here are the products ONE is looking to implement in these rooms:

(source)

Today’s update confirmed that this is still progressing:

“This health system has over 85 hospitals and over 15,000 beds and is now in direct negotiations with Oneview over the scope and timing of the initial project for this health system.”

(source)

For context at the end of CY2025, ONE had 14,880 live endpoints across its existing customer base (an endpoint is basically a connected device that ONE is able to charge for).

So a single Top 10 health system rolling out across its network has the potential to be material relative to ONE’s installed base.

There’s of course no guarantee the negotiations will result in the full system getting deployed.

But the conversation has now started, and we’re hoping to see initial purchase orders flow over the coming quarters.

Our take on the financials:

The big change this quarter was the capital raise ONE completed.

ONE completed a two-tranche placement of CDIs to institutional and sophisticated investors raising a total of A$19M (~€11.4M).

Tranche 2 (A$7M / ~€4.2M) is subject to shareholder approval and ONE is going to seek that approval at its AGM in September 2026 rather than calling a separate EGM (saving cost).

ONE also completed a SPP that closed 10 April and was finalised 17 April, raising a further A$300k with all valid applications accepted in full.

(These proceeds aren’t in the 31 March cash balance as they landed after the quarter ended.)

So ONE went into the quarter with €4.6M cash and it came out with €10.3M cash, with another A$7M still to come once the AGM ticks off Tranche 2.

We like the ONE took the opportunity to take the cash when it was available - which will give ONE a balance sheet to go hard on maxing out Ai use across the business.

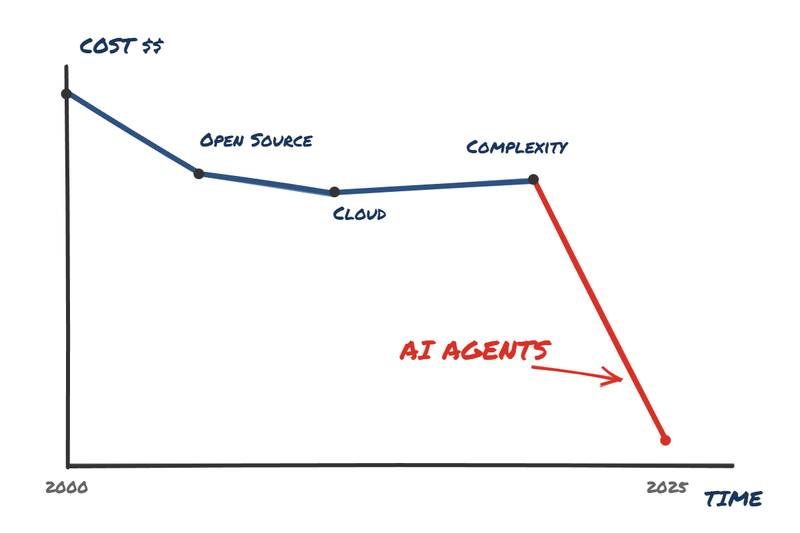

One chart that lives rent free in our head is the following - which makes us think ~A$19M can go a lot further now with ONE then it has in the past…

(source - a visual showing how AI MAY have changed software dev costs)

We covered this in our deep dive article following us taking part in the raise in mid March: ONE: Med Tech into 18 new US hospitals and a sales pipeline of ~€53M in potential recurring revenue.

The place it will be most applicable is ONE’s “Ovie”, it’s AI assistant product/technology:

(source)

The way ONE is positioning Ovie:

- It builds on the voice assistant introduced in 2025

- It’s being developed as an orchestration layer for non-clinical workflows - patient self-service, request routing, operational visibility for care teams

- ONE plans pilot deployments with selected customers during 2026

- The redesigned patient user interface that underpins the Ovie ecosystem is expected to be commercially available in the second half of 2026

This is the AI angle to ONE’s product story and a large part why we took part in the raise so the pilot deployments through 2026 are what we’ll be watching to validate the workflows ahead of its rollout.

What do we expect ONE to deliver?

Sales pipeline conversion into signed contracts

ONE had 180+ opportunities and 48,000+ endpoints in its sales pipeline when last provided. We want to see this translate into new signed deals, new customer logos, and accelerating endpoint growth.

Milestones we are tracking:

- ✅ Added to GPO of top-10 US hospital network (January 2026)

- 🔄 First hospital wins from the Top 10 US hospital Group Purchasing Organisation network (confirmed progressing)

- 🔲 New logo wins.

- 🔲 Installed beds converted into multiple “endpoints”.

Rollout of “Ovie” AI services

We want to see the Ovie AI product suite move from announcement to live deployment and start contributing to per-endpoint revenue uplift.

Milestones we are tracking:

- ✅ Ovie digital care assistant unveiled

- 🔲 Ovie customer trials (to begin this year with full rollout during late 2026)

- 🔲 New user experience delivered (H2 2026)

- 🔲 First Ovie-related revenue contribution

Revenue growth and path to breakeven

We want to see ONE continue its consistent growth trajectory and demonstrate a clear path to operating cash flow breakeven.

Milestones we are tracking:

- 🔄 CY2026 live deployment growth of 20% (~17,850 endpoints per guidance)

- 🔄 Continued decline in cash OpEx through 2026

- 🔲 Breakeven achieved